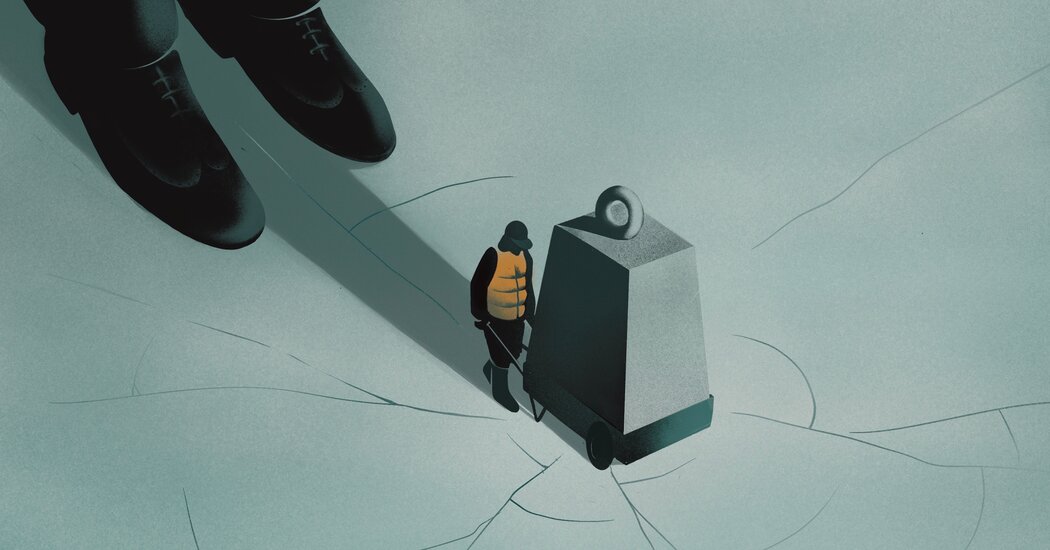

WASHINGTON – Developing countries face a catastrophic debt crisis in the coming months due to rapid inflation, slow growth, high interest rates and strengthening the dollar They combine into a perfect storm that could lead to a chaotic wave of defaults and inflict economic pain on the world’s most vulnerable people.

Poor countries owe, by some accounts, up to $200 billion to rich countries, multilateral development banks and private creditors. Rising interest rates increased the value of the dollar, making it difficult for foreign borrowers owed in US currency to repay their loans.

Defaulting on a huge batch of loans would raise borrowing costs for vulnerable countries and could lead to financial crises when they occur. Almost 100 million people have already been pushed into poverty This year through the combined effects of the pandemic, inflation and the Russian war in Ukraine.

The risk is another headwind for the global economy, which was heading towards recession. Leaders of the world’s advanced economies have been privately grappling in recent weeks over how to avoid financial crises in emerging markets like Zambia, Sri Lanka and Ghana, but have struggled to develop a plan to accelerate debt relief as they grapple with their own economy. woes.

As rich countries brace for a global recession and try to cope with rising food and energy prices, investment flows to the developing world are easing and major creditors, in particular Chinahas been slow to restructure loans.

Mass defaults in low-income countries are unlikely to trigger a global financial crisis given the relatively small size of their economies. But the potential is forcing policymakers to rethink debt sustainability in an era of rising interest rates and increasing opacity of loan transactions. In part, this is because defaults can make it more difficult for countries like the United States to export goods to heavily indebted countries, further slowing the global economy and potentially leading to widespread hunger and social unrest. With Sri Lanka on the verge of default this year, its central bank has been forced to Arrange a barter agreement To pay for Iranian oil with tea leaves.

“Finding ways to reduce debt is important for these countries until they get to the light at the end of the tunnel,” David Malpass, president of the World Bank, said in an interview at the G-20 summit last month in Bali. , Indonesia. “This burden on developing countries is heavy, and if it continues, it continues to worsen, which then affects the developed economies in terms of increased migration flows and lost markets.”

The urgency comes in the wake of coronavirus lockdowns in China and Russia’s war in Ukraine, which have crimped global production and sent food and energy prices soaring. The Federal Reserve was rapidly raising interest rates in the United States, Strengthening the dollar and increasing the cost of importing necessities to developing countries for a population already suffering from high prices.

Economists and global financial institutions such as the World Bank and the International Monetary Fund have been sounding the alarm about the seriousness of the crisis. The World Bank predicted this year that approx dozens of countries It could face default next year, and the IMF has calculated that 60 percent of developing countries are low-income They are in debt distress or are in great danger.

Since then, the financial conditions of developing countries have continued to deteriorate. The Council on Foreign Relations said last week that 12 countries now have the highest default rating, up from three 18 months ago.

Frequently asked questions about inflation

What is inflation? Inflation is a Loss of purchasing power over time, which means your dollar will not go tomorrow the way it did today. It is usually expressed as the annual change in the prices of everyday goods and services such as food, furniture, clothing, transportation, and toys.

Brad Setser, a senior fellow on the council, estimates that $200 billion of emerging market sovereign debt needs to be restructured.

“It is certainly a systemic problem for the affected countries,” Mr. Setser said. “Because an extraordinarily large number of countries borrowed from the market and borrowed from China between 2012 and 2020, there are an extraordinarily large number of countries that are in default or at risk of default.”

Debt restructuring can include providing grace periods for repayment, lowering interest rates, and forgoing some of the principal amount owed. The US has traditionally led large-scale debt relief initiatives such as the Brady Bond plan for Latin America in the 1990s. However, the emergence of high-rate commercial creditors and copious loans from China—which was loath to take losses—complicated international debt relief efforts.

Fitch, the credit rating company, warned in a report last month of “the potential for more defaults” in emerging markets next year, and lamented that the so-called common framework set up by the G-20 in 2020 to facilitate debt restructuring “does not prove Effective in resolving crises quickly.

Since the framework was put in place, only Zambia, Chad, and Ethiopia have sought debt relief. It has been an excruciating process, involving creditor committees, the International Monetary Fund and the World Bank, all of which must negotiate and agree on how to restructure the loans that countries owe. After two years, Zambia is finally on the verge of restructuring its debt to state banks in China, and Chad reached an agreement last month with private creditors, including Glencore, to restructure its debt.

Bruno Le Maire, France’s finance minister, said progress with Zambia and Chad was a positive step, but that there was a lot of work to be done with other countries.

“Now we must hurry,” Mr. Le Maire said on the sidelines of the G-20 summit.

China, which has become one of the world’s largest creditors, remains an obstacle to relief. It has been accused by development experts of setting “debt traps” for developing countries through a lending program of more than $500 billion, which has been described as predatory.

“This is really about China’s unwillingness to admit that its lending was unsustainable, that China is slowing down on deals,” said Mark Sobel, a former Treasury official and US president of the Official Monetary and Financial Institutions Forum.

The United States has regularly urged China to be more accommodating, and complained that it is difficult to restructure Chinese loans because of the opaque terms of the contracts. He described China’s lending practices as “unconventional”.

Brent Neiman, advisor to Treasury Secretary Janet L. “But across the international lending landscape, China’s lack of participation in coordinated debt relief is more common and more significant.”

China has accused Western commercial creditors and multilateral institutions of failing to do enough to restructure debts and has denied engaging in predatory lending.

“These are not ‘debt traps’, but traces of cooperation,” said Wang Yi, China’s foreign minister, He said this year.

China’s economy is slowing due to its strict “zero Covid” policy, which has included mass testing, quarantine and lockdown of its population. The domestic real estate crisis also made it difficult for China to accept the loan losses it extended to other countries.

IMF officials will travel to Beijing next week for a “1+6” round table with leaders of major international economic institutions. During those meetings, they will help China better understand the debt restructuring process through the common framework.

Ceyla Pazarbasioglu, director of the International Monetary Fund’s Strategy, Policy and Review Division, acknowledged that approval of debt relief terms may take time, but said she would convey the urgency to Chinese officials.

“The problem we have is that we don’t have time now because countries are too fragile to deal with debt vulnerability,” Ms. Pazarbasioglu, who will be traveling to China, told reporters at the International Monetary Fund last week.

At the annual meetings of the International Monetary Fund and the World Bank in Washington in October, policymakers said the pace of debt restructuring was too slow and called for coordinated action between creditors and borrowers to find solutions before it is too late.

During a panel discussion on debt restructuring, Gita Gopinath, Senior Deputy Managing Director of the International Monetary Fund, said countries and creditors need to avoid the kind of wishful thinking that has led to defaults.

“There is a great tendency to gamble for salvation,” Mrs. Gopinath said. “There is a great tendency for creditors to hope there is a gamble for redemption, and then nothing gets resolved.”

But in conclusion G20 meeting In November, little progress appeared to be made. In a joint declaration, the leaders expressed concern about the “deteriorating debt situation” in some vulnerable middle-income countries. However, they offered few concrete solutions.

“We reaffirm the importance of joint efforts by all actors, including private creditors, to continue working towards enhancing debt transparency,” the statement read.

The statement included a footnote saying that “one member has divergent views on debt issues”. That country, according to people familiar with the matter, is China.

In the interview, Mr. Malpass said that China has been willing to discuss debt relief, but that “the devil is in the details” when it comes to restructuring loans to reduce debt burdens.

The World Bank chief predicted that the financial problems facing developing countries are unlikely to turn into a global debt crisis of the kind that occurred in the 1980s, when many Latin American countries were unable to service their external debts. However, he noted that there is a moral imperative to do more to help poor countries and populations that have been further impoverished during the pandemic.

“There will be continuing setbacks in development in terms of poverty and hunger and malnutrition, which are already on the rise,” said Mr. Malpass. “It comes at a time when countries need more resources, not less.”

{kind=link}